Règlement de conformité visant à encourager l'utilisation de la signature électronique pour les prêts hypothécaires

Les entreprises dans une variété de secteurs ont beaucoup de raisons de mettre en œuvre des logiciels de signature électronique. Cependant, certaines organisations ont besoin de quelque chose pour servir de catalyseur pour les faire connaître de leurs préoccupations initiales et se plonger dans la nouvelle technologie.

Ce catalyseur peut avoir surgi pour les prêteurs hypothécaires, comme de nouveaux règlements ont fait l'adoption de signature électronique une option extrêmement attrayante. Selon un récent rapport du New York Times, les questions liées aux applications poussent les prêteurs à commencer à mettre en œuvre la technologie de signature électronique.

Les signatures électronique améliorent la conformité pour les prêteurs

Les nouvelles lois sur les demandes qui entrent en vigueur en août 2015 stipulent que les prêteurs répondent à certaines demandes de divulgation de clients dans les trois jours, a expliqué la source de nouvelles. Par exemple, toute demande relative à l'estimation des coûts doit être répondue dans le nouveau délai de trois jours. Les prêteurs hypothécaires doivent non seulement répondre à ces demandes, ce qui peut présenter certains défis de processus, ils doivent également être en mesure de documenter qu'ils ont respecté ces lignes directrices.

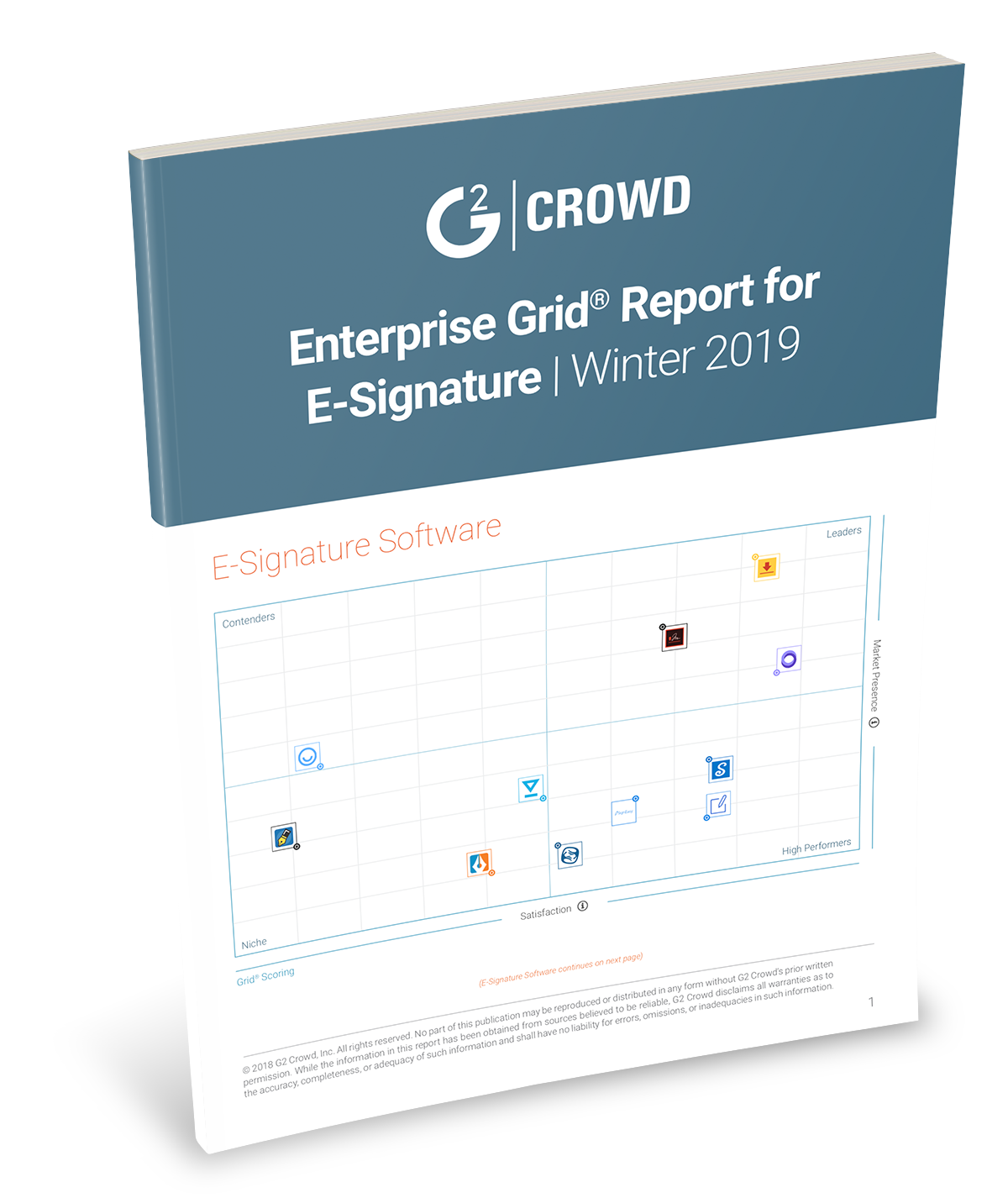

G2 CROWD'S ELECTRONIC SIGNATURE SOFTWARE RANKINGS

C'est le 12ede G2 Crowd, et le rapport de classement le plus détaillé de signature électronique. Il confirme OneSpan Sign comme le leader de la satisfaction de la clientèle avec le plus haut score NPS (83) pour la deuxième fois consécutive.

TÉLÉCHARGER LE RAPPORT MAINTENANTL'expert de l'industrie Kelli Himebaugh a expliqué en détail comment les nouveaux processus de demande ont un impact sur l'utilisation de la signature électronique parmi les prêteurs.

« À l'heure actuelle, aujourd'hui, il y a une large adoption des signatures électroniques et de la livraison électronique des documents de divulgation initiale dans le cadre du processus de demande », a déclaré Himebaugh au New York Times. « Vous devez être en mesure de suivre que les emprunteurs ont reçu ces documents dans les trois jours, ce qui aide à prouver la conformité. »

La politique de signature électronique peut également aider les prêteurs à alléger les divers fardeaux qui sont associés à la transmission de documents aux clients. Toute transaction hypothécaire implique beaucoup de paperasse qui peut être écrasante pour les prêteurs et les clients. Cela crée un ensemble de tâches longues et sujettes aux erreurs qui peuvent générer des inefficacités et des coûts pour les prêteurs.

Il peut également ajouter de la confusion pour les prêteurs. Selon le rapport, le nouveau règlement exigera également que les prêteurs obtiennent des documents de clôture aux clients dans les trois jours suivant la fermeture, établissant un autre scénario dans lequel les signatures électronique deviennent de plus en plus importantes.

Utilisation des signatures électroniques dans le cadre des plans réglementaires

De nombreux règlements dans un large éventail de secteurs exigent que les organisations trouvent des moyens de documenter leurs processus et de s'assurer que les autorisations appropriées sont en place. Les solutions de signature électronique jouent un rôle essentiel dans les stratégies de conformité parce qu'elles permettent aux organisations de documenter automatiquement diverses opérations, y compris lorsque des documents sont envoyés aux utilisateurs, lorsque les individus ouvrent des contrats et combien de temps ils passent différentes pages du dossier.

Ce processus de documentation peut être établi de manière à authentifier les utilisateurs et à enclendre l'ensemble du processus de signature électronique, en protégeant les entreprises et leurs clients tout en assurant la conformité réglementaire.