VASCO Reports Results for Fourth Quarter and Full-year 2015

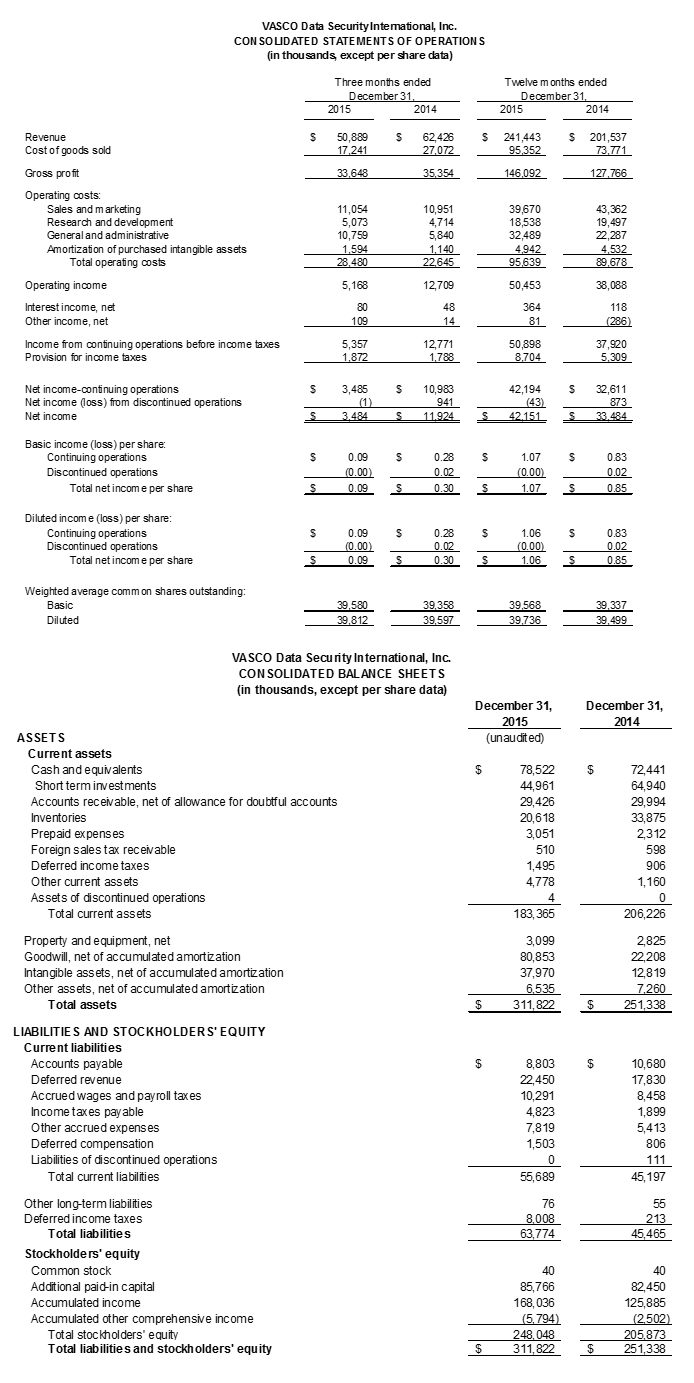

Revenue from continuing operations for the fourth quarter and full-year 2015 was $50.9 million and $241.4 million, respectively, a decrease of 18% compared to the fourth quarter of 2014 and an increase of 20% compared to full-year 2014. Operating income from continuing operations for the fourth quarter and full-year 2015 was $5.2 million and $50.5 million, respectively, a decrease of 59% compared to the fourth quarter of 2014 and an increase of 32% compared to the full-year 2014. Financial results for the periods ended December 31, 2015 and guidance for full-year 2016 to be discussed on conference call today at 4:30 p.m. ET.

OAKBROOK TERRACE, IL, and ZURICH, February 16, 2016 - VASCO Data Security International, Inc. (NASDAQ: VDSI), today reported financial results for the fourth quarter and full-year ended December 31, 2015.

Revenue from continuing operations for the fourth quarter of 2015 decreased 18% to $50.9 million from $62.4 million in the fourth quarter of 2014, and for the full-year 2015, increased 20% to $241.4 million from $201.5 million in 2014.

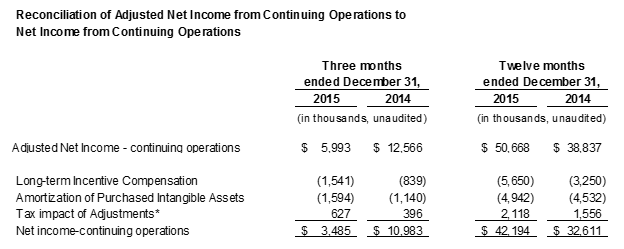

Net income from continuing operations for the fourth quarter of 2015 was $3.5 million, or $0.09 per fully diluted share, a decrease of $7.5 million, or 68% from $11.0 million, or $0.28 per fully diluted share, for the fourth quarter of 2014. Net income from continuing operations for the full-year 2015 was $42.2 million, or $1.06 per fully diluted share, an increase of $9.6 million, or 29%, from $32.6 million, or $0.83 per fully diluted share for the full-year 2014.

Net income, which includes the impact of our discontinued operations, was $3.5 million, or $0.09 per diluted share and $42.2 million or $1.06 per diluted share for the fourth quarter and full-year 2015, respectively. Net income for the fourth quarter and full-year 2014 was $11.9 million, or $0.30 per diluted share and $33.5 million, or $0.85 per diluted share, respectively.

On November 25, 2015, VASCO completed its acquisition of Silanis Technology, Inc., a leading provider of e-signature solutions used to sign, send and manage documents. VASCO believes the acquisition will allow it to deliver new solutions that are in high demand and accelerate its transition to a recurring revenue model, among other benefits. Results for Silanis, following the closing of the acquisition, are included in fourth quarter and full-year 2015 results, more fully described in “Other Financial Highlights.”

-

Gross profit from continuing operations was $33.6 million or 66% of revenue for the fourth quarter of 2015 and $146.1 million or 61% of revenue for the full-year 2015. Gross profit was $35.4 million and $127.8 million for the fourth quarter and the full-year 2014, respectively, which was 57% and 63% of revenue, respectively.

-

Operating expenses from continuing operations for the fourth quarter and full-year 2015 were $28.5 million and $95.6 million, respectively, an increase of 26% from $22.6 million reported for the fourth quarter of 2014 and an increase of 7% from $89.7 million reported for the full-year 2014. Operating expenses from continuing operations for the fourth quarter and full-year 2015 include transaction fees related to the Silanis acquisition of $1.9 million and $2.4 million, respectively and expenses of $1.5 million and $2.7 million, respectively, related to our internal investigation of the possible sale of our products by a distributor into Iran.

-

Operating income from continuing operations for the fourth quarter and full-year 2015 was $5.2 million and $50.5 million, respectively, a decrease of $7.5 million, or 59%, from $12.7 million reported for the fourth quarter of 2014 and an increase of $12.4 million, or 32%, from $38.1 million reported for the full-year 2014. Operating income from continuing operations, as a percentage of revenue, was 10% and 21% for the fourth quarter and full-year 2015, respectively, compared to 20% and 19% for the comparable periods in 2014. Operating income from continuing operations for the fourth quarter included Silanis post acquisition operating loss of $2.5 million.

-

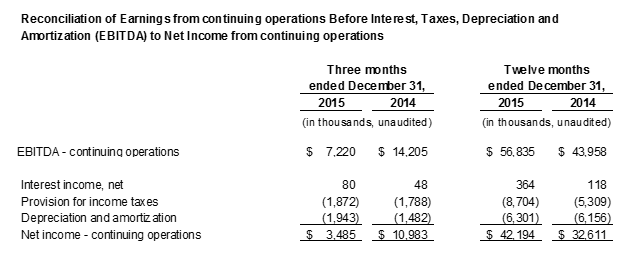

Earnings before interest, taxes, depreciation and amortization (EBITDA) from continuing operations was $7.2 million and $56.8 million for the fourth quarter and full-year 2015, respectively, a decrease of 49% from $14.2 million reported for the fourth quarter of 2014 and an increase of 29% from $44.0 million reported for the full-year 2014.

-

Cash, cash equivalents and short-term investments at December 31, 2015 totaled $123.5 million compared to $184.0 million and $137.4 million at September 30, 2015 and December 31, 2014, respectively. There were no bank borrowings at any of the periods ended December 31, 2015, September 30, 2015 or December 31, 2014.

-

VASCO announced two solutions targeting the rapidly growing healthcare segment; DIGIPASS Authentication for Epic Hyperspace, a plug-in for IDENTIKEY Authentication Server; and DIGIPASS GO 7, a one-button hardware authenticator that has been validated as FIPS 140-2 Level 2 compliant by the federal National Institute of Standards and Technology (NIST).

-

Mark Hoyt, former Groupon EMEA CFO, joined VASCO and commenced serving as Chief Financial Officer, Secretary and Treasurer as of November 4, 2015.

VASCO is providing guidance for the full-year 2016 as follows:

-

Revenue is expected to be in the range of $205 million to $215 million, and

-

Operating income as a percentage of revenue, excluding the amortization of purchased intangible assets, is projected to be in the range of 10% to 12%.

"Our results for the fourth quarter were solid and our full-year revenue for 2015 was the best in the Company’s history,” stated T. Kendall Hunt, Chairman & CEO. “Implementing multifactor authentication against criminal and state-sponsored hacking attacks has become a necessity for every businesses and this continues to be a significant contributor to our growth. During 2015, we continued to extend our leadership position through the introduction of innovative anti-fraud solutions. Enhancements to our product line during 2015 included, but were not limited to, additional products featuring our Cronto technology, Runtime Application Self-Protection (RASP) capabilities in our DIGIPASS for Apps mobile application security library, the IDENTIKEY Risk Manager comprehensive risk management solution, and a FIPS 140-2 level 2 certified authenticator engineered to meet the strict regulatory requirements of the healthcare market. We completed the acquisition of Silanis Technology, Inc., a leading provider of e-signature solutions bringing VASCO a new product category that is already in high demand among our customers and that allows us to accelerate our transition to a recurring revenue model and expand our customer base into additional verticals. Our continuing strong performance and ability to generate cash will facilitate additional acquisitions that we expect will contribute to future revenue growth. For 2016, we will continue to deliver growth in strategic areas while maintaining positive operating results that reflect our commitment to the proper balance of growth and financial stability.

“Our operating performance in 2015 demonstrated our strength and stability," said Jan Valcke, VASCO's President and COO. "The results for the full-year 2015 reflected a 20% increase in revenue. Gross margin for the fourth quarter of 2015 was 66%, returning to the historic levels of previous few years as the mix of products sold shifted back to higher margin authenticators and software solutions. We believe we are making substantial progress with important proofs of concept with large customers that will help drive future revenue. Many of these projects are for our new solutions, Cronto and DIGIPASS for Apps. We anticipate significant growth in our software solutions revenue in 2016 and we believe that substantially all of this revenue will be incremental to our hardware revenue. We are well positioned in the market with the optimal mix of durable customer relationships, strong demand for our solutions, and a unique technology platform that is not available from competitors.”

In conjunction with this announcement, VASCO Data Security International, Inc. will host a conference call today, February 16, 2016, at 4:30 p.m. EST - 22:30h CET. During the conference call, Mr. Ken Hunt, CEO, Mr. Jan Valcke, President and COO, and Mr. Mark Hoyt, CFO, will discuss VASCO’s results for the fourth quarter and full-year 2015 and guidance for full-year 2016.

To participate in this conference call, please dial one of the following numbers:

USA/Canada: 1 800 676 3079

International: +1 303 223 4385

Mention VASCO to be connected to the Conference Call.

The Conference Call is also available in listen-only mode on www.vasco.com. Please log on 15 minutes before the start of the Conference Call in order to download and install any necessary software. The recorded version of the Conference Call will be available on the VASCO website 24 hours a day for at least 60 days.

VASCO is a world leader in providing two-factor authentication and digital signature solutions to financial institutions. Many of the top 100 global banks rely on VASCO solutions to enhance security, protect mobile applications and meet regulatory requirements. VASCO also secures access to data and applications in enterprise environments, and provides tools for application developers to easily integrate security functions into their web-based and mobile applications. VASCO enables more than 10,000 customers in 100 countries to secure access, manage identities, verify transactions, and protect assets across financial, enterprise, E-commerce, government and healthcare markets. Learn more about VASCO at vasco.com and on Twitter, LinkedIn and Facebook.

This press release contains forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934 and Section 27A of the Securities Act of 1933, including, without limitation the guidance for full year 2016. These forward-looking statements (1) are identified by use of terms and phrases such as “expect”, “believe”, “will”, “anticipate”, “emerging”, “intend”, “plan”, “could”, “may”, “estimate”, “should”, “objective”, “goal”, “possible”, “potential”, “project” and similar words and expressions, but such words and phrases are not the exclusive means of identifying them, and (2) are subject to risks and uncertainties and represent our present expectations or beliefs concerning future events. VASCO cautions that the forward-looking statements are qualified by important factors that could cause actual results to differ materially from those in the forward-looking statements. These risks, uncertainties and other factors that have been described in our Annual Report on Form 10-K for the year ended December 31, 2014 and include, but are not limited to, (a) risks of general market conditions, including currency fluctuations and the uncertainties resulting from turmoil in world economic and financial markets, (b) risks inherent to the computer and network security industry, including rapidly changing technology, evolving industry standards, increasingly sophisticated hacking attempts, increasing numbers of patent infringement claims, changes in customer requirements, price competitive bidding, and changing government regulations, and (c) risks specific to VASCO, including, demand for our products and services, competition from more established firms and others, pressures on price levels and our historical dependence on relatively few products, certain suppliers and certain key customers. These risks, uncertainties and other factors include VASCO’s ability to integrate Silanis into the business of VASCO successfully and the amount of time and expense spent and incurred in connection with the integration; the risk that the revenue synergies, cost savings and other economic benefits that VASCO anticipates as a result of the Acquisition are not fully realized or take longer to realize than expected. Thus, the results that we actually achieve may differ materially from any anticipated results included in, or implied by these statements. Except for our ongoing obligations to disclose material information as required by the U.S. federal securities laws, we do not have any obligations or intention to release publicly any revisions to any forward-looking statements to reflect events or circumstances in the future or to reflect the occurrence of unanticipated events.

Non-GAAP Financial Measures

The Company reports its financial results in accordance with GAAP, but Company management also evaluates its performance using EBITDA, Adjusted Net Income and Adjusted Diluted EPS. The Company’s management believes that these measures provide useful supplemental information regarding the performance of our business and facilitates comparisons to our historical operating results.

These non-GAAP measures are not measures of performance under GAAP and should not be considered as alternatives or substitutes for the most directly comparable financial measures calculated in accordance with GAAP. While we believe that these non-GAAP measures are useful within the context described below, they are in fact incomplete and are not a measure that should be used to evaluate our full performance or our prospects. Such an evaluation needs to consider all of the complexities associated with our business including, but not limited to, how past actions are affecting current results and how they may affect future results, how we have chosen to finance the business, and how taxes affect the final amounts that are or will be available to shareholders as a return on their investment.

EBITDA

We define EBITDA as net income from continuing operations before interest, taxes, depreciation and amortization. We use EBITDA as a simplified measure of performance for use in communicating our performance to investors and analysts and for comparisons to other companies within our industry. As a performance measure, we believe that EBITDA presents a view of our operating results that is most closely related to serving our customers. By excluding interest, taxes, depreciation and amortization we are able to evaluate performance without considering decisions that, in most cases, are not directly related to meeting our customers’ requirements and were either made in prior periods (e.g., depreciation and amortization), or deal with the structure or financing of the business (e.g., interest) or reflect the application of regulations that are outside of the control of our management team (e.g., taxes). Similarly, we find that the comparison of our results to those of our competitors is facilitated when we do not need to consider the impact of those items on our competitors’ results.

Adjusted Net Income & Adjusted Diluted EPS

We define Adjusted Net Income and Adjusted Diluted EPS, as net income or EPS from continuing operations before the consideration of long-term incentive compensation expenses and the amortization of purchased intangible assets. We use these measures to assess the impact of our performance excluding items that though they are recurring, can significantly impact the comparison of our results between periods and the comparison to competitors.

Long-term incentive compensation for management and others is directly tied to performance and this measure allows management to see the relationship of the cost of incentives to the performance of the business operations directly if such incentives are based on that period’s performance. To the extent that such incentives are based on performance over a period of several years, there may be periods which have significant adjustments to the accruals in the period but which relate to a longer period of time, and which can make it difficult to assess the results of the business operations in the current period. In addition, the Company’s long-term incentives generally reflect the use of restricted stock grants or cash awards while other Companies may use different forms of incentives the cost of which is determined on a different basis, which makes a comparison difficult.

The Company also excludes amortization of purchased intangible assets because it believes that the amount of such expenses in any given period may not be correlated directly to the performance of the business operations and that such expenses can vary significantly between periods as a result of new acquisitions, the full amortization of previously acquired intangible assets or the write down of such assets due to an impairment event.

This document may contain trademarks of VASCO Data Security International, Inc. and its subsidiaries, including VASCO, the VASCO “V” design, DIGIPASS, VACMAN, aXsGUARD, Cronto and IDENTIKEY.

For more information contact:

John Gunn

+1-847-370-1486

[email protected]