Why European banks must act now on EUDI Wallets: Regulatory drivers, deadlines, and current ambiguities

Learn about the requirements, regulations, and major deadlines for banks to adopt EUDI Wallets for...

PSD3 updates: Deep dive on fraud prevention, bank liability, and the regulatory impact

Get PSD3 PSR updates today to prepare your compliance. Learn about bank liability, news for PSPs, and...

The Authentication Newsletter for January 2026

Explore 2026 predictions, regulatory updates, fraud prevention tips, the future of authentication, and...

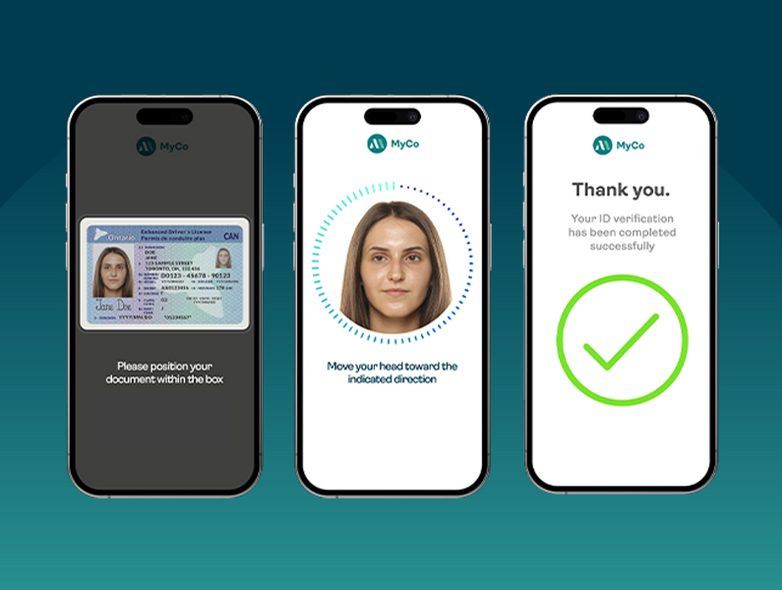

FINTRAC: Preparing your identity verification strategy for more than just compliance

FINTRAC-ready vs FINTRAC-optimized? Learn how the right approach to identity verification facilitates...

Passkeys implementation: Build or buy?

Passkey authentication offers strong security benefits, but should you build or buy? Explore 6 key...

Pros and cons of passkeys: Security benefits outweigh risks

Don’t overlook passkeys due to rare risks. Discover how they deliver stronger security and more seamless...

Beyond authentication: Why device and behavioral intelligence are now non-negotiable for banks

To combat modern payment fraud schemes and meet regulatory requirements, banks need to implement device...

FINTRAC’s identity verification guidance is a timely step forward—but compliance will require legwork

As FINTRAC rolls out an extension of its anti-money laundering and anti-terrorist financing requirements...