American Banker surveys the state of digital readiness in banking

Wherever your banking organization is in its digital document and automation processes, you can take steps toward a less manual future.

While recent abrupt social and economic changes have necessitated that all banks and credit unions make progress on digitizing internal and/or customer-facing agreements, not all organizations in the banking sector have advanced at the same pace towards digital banking. Some banks are farther along in their initiatives toward a fully automated, secure agreement system and customer experience. Their actions provide a learning opportunity for other banking organizations.

Based on a 2022 survey of 141 management-level respondents in the banking industry, we’ve segmented banks and credit unions into four groups determined by digital readiness when it comes to agreement automation. They are:

- Just Getting Started

- Cautiously Advancing

- Keeping Pace with Your Peers

- Leading the Way

The research, conducted by Arizent/American Banker and sponsored by OneSpan, offers insights for bank professionals at all stages of the agreement automation process and digital transformation journey.

Survey Results on Digital Transformation in Banking

Usage of a forms automation solution to digitize agreements

59% of respondents are using form automation for specific use cases or scaling out applicable use cases enterprise-wide to digitize internal and/or customer-facing agreements (e.g., account opening agreements, loan applications, vendor contracts, etc.). When we dig deeper, we see a clear difference between leaders and those just getting started. 40% of leaders have already fully executed on forms automation for all planned use cases versus 0% in the getting started category. Further, 60% of leaders are scaling out their solution for all applicable use cases enterprise-wide versus 8% of those getting started.

The takeaway: If your organization hasn’t implemented e-forms to automate the digital agreements process, now is the time to make this a priority. For those that are at some stage of implementation, consider the next steps in your digital transformation strategy, such as actively piloting or using e-forms on a limited basis for specific use cases.

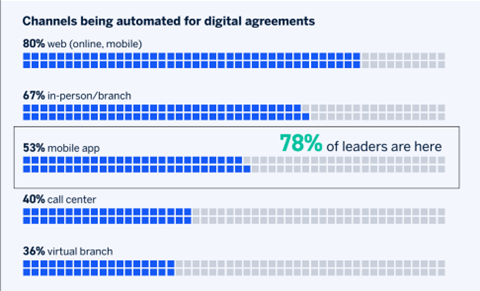

Channels in which the delivery and execution of digital agreements is being automated

Looking at the full data set for all participants, web (online/mobile banking) is the most automated channel followed by in-person branch then mobile app. With leaders, we see that 100% of respondents have automated the delivery and execution of digital agreements on the web, followed by in-person branch (90%), mobile app (80%), call center (70%), and virtual branch (50%). Contrast those numbers with the responses of those just getting started: web (50%), mobile app (27%), in-person branch (23%), call center (19%), and virtual branch (4%).

The takeaway: To take full advantage of the benefits of a digital process, consider implementing electronic signature, e-forms, identity verification, authentication, and other digital technologies in more channels.

Usage of eSignatures in agreement processes

56% of respondents report using e-signatures for specific use cases or scaling out applicable use cases enterprise-wide. Looking deeper, we see that leaders are quite ahead here, with 70% having fully executed for all planned use cases and 30% scaling out for all applicable use cases enterprise-wide. Those getting started, however, are at 8% and 4% for the same categories.

The takeaway: The usage of e-signatures streamlines and optimizes business processes. Neo-banks and traditional banking organizations alike benefit from making full use of this technology wherever signatures are needed.

Methods used to securely verify users’ identities before they access and sign digital agreements

The top approaches used by respondents include ID document verification, two-factor authentication (2FA) and one-time passcodes (OTP).

These three cybersecurity strategies are also the top ones for leaders (70% for each), with PINs and passwords also at 70%, followed by knowledge-based authentication (KBA) at 50% and email authentication at 40%. When we consider those just getting started, we see opportunities to improve on verification: ID document verification (32%), two-factor authentication (20%), one-time passcodes (20%), and email authentication (20%).

The takeaway: In Web3, authentication and identity verification need to be continuous to stay ahead of identity fraud. This means organizations must develop accurate-and reliably-reproduced audit trail capabilities for all interactions as well as proving the identity of participants in an agreement. With digital attacks, fraud attacks, and cybercrime so commonplace, organizations must ensure the people involved in a digital agreement are in fact the legitimate customers.

Improving completion rates/reducing abandonment

While 40% of respondents say their current digital agreement process is extremely or very effective at improving completion rates, the number for leaders is double that (80%). On the other hand, only 12% of those just getting started report this level of effectiveness.

The takeaway: Look to your peers leading the way for automation strategies to help you make your processes more effective at improving completion rates and reducing abandonment. This is the perfect place to talk about how one insurance company increased completions and to link to that case study as an example of a peer leading the way!

Ensuring compliance and non-repudiation

While 65% of respondents say their current digital agreement process is extremely or very effective at ensuring compliance, only 12% of those getting started say the same. For their part, however, leaders report 90% extremely/very effective when it comes to this topic.

The takeaway: No matter where you are in your digital agreement automation process, you can look to leaders on things like use of e-signatures and user identity verification methods to help your organization improve compliance and non-repudiation.

Readiness checklist: How to get started with eSignatures

Learn the various implementation options as well as the top technical requirements to deploying electronic signatures in your organization.

Methodology

This research was conducted online from May through September 2022 among 141 management-level respondents in the banking industry. Respondents are employed by retail/commercial banks, credit unions, tech vendors/fintech companies and challenger/online banks.