How Digital Identity Verification Can Help Prevent Application Fraud in Real-Time

By 2020, it is projected that U.S. financial institution (FI) spending to combat account application fraud losses will reach US$599 million. Bank account application fraud occurs when a fraudster uses either stolen personal identifiable information (PII) or synthetic ID documents to open a new bank account – trying to pass as a legitimate first-time customer.

Application and Identity Fraud Prevention: A Balancing Act

Instances of application and identity fraud are highly damaging for financial institutions and are being fueled, in part, by over 13 billion data records that have been lost or stolen since 2013. After first-party fraud (when an individual, or group of people, intentionally misrepresent their identity or give false information), stolen data obtained through data breaches are one of the top three causes of application fraud.

To prevent application fraud, financial institutions must successfully identify fraudulent activity or fraudulent identity documents in real-time at the beginning of the new account opening process. At the same time, FIs are also under pressure to digitize account openings so customers can open an account entirely online or via a mobile device. Recent research shows the extent of these pressures, especially among younger demographics – with 37% of consumers and 57% of millennials stating that they would prefer to open a new account online.

To achieve a successful fraud prevention strategy, banks must conduct a balancing act between security and customer experience. Banks need to put in place an account opening process that includes real-time risk assessment and identity verification, while delivering a digitally seamless customer experience. The importance of improving the customer experience cannot be understated. 88% of FIs state that improving the customer onboarding experience is very important as they make technology investments.

With the right solution, banks can have the best of both worlds. To show how OneSpan approaches this balancing act, we’re going to walk through a typical first-time digital account opening experience.

Opening a New Bank Account Online or via a Mobile Device

As we walk through this digital account opening process, we have included screenshots of the relevant desktop and mobile customer-facing interfaces to demonstrate the customer experience. Additionally, we will also describe what the solution is doing behind the scenes to help prevent application fraud. Though this blog presents a mobile scenario, a browser-based banking application with account opening capabilities can also provide the same seamless experience.

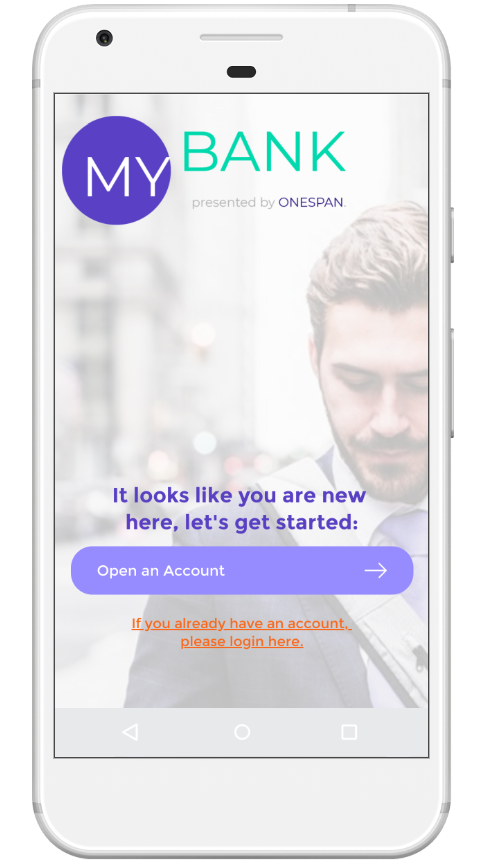

First, we need our customer. Let’s suppose a potential customer, Holly, is switching to a new bank and wants to open a new savings account on the bank’s website on her mobile phone. Her first step is to visit the bank’s website and select “Open an Account” to begin the process.

Digital Identity Verification Prevents Identity Fraud

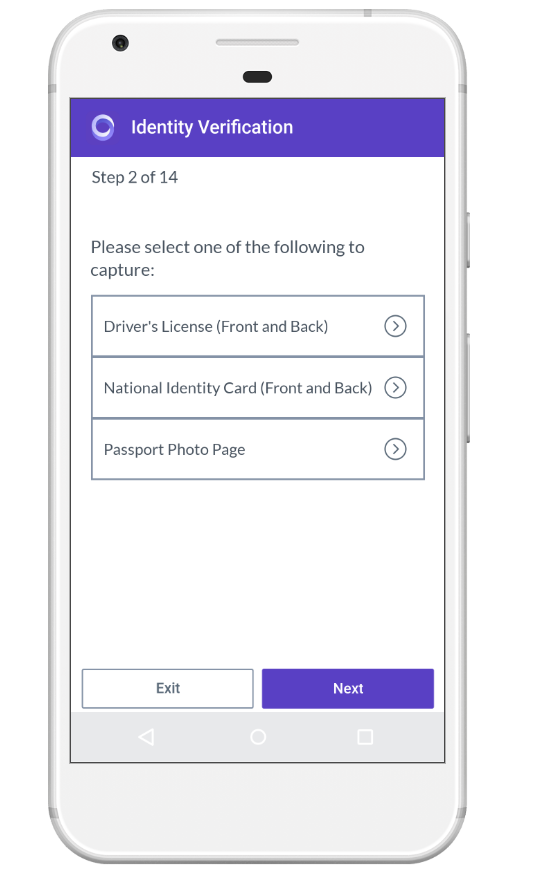

Since Holly is opening her new account remotely (not in bank or branch), she is asked to verify her identity digitally by scanning both the front and back of her driver’s license or government-issued ID with the camera on her mobile device.

This is the point where application fraud is most likely to occur. Catching it at the beginning of the new account application stage by identifying fraudulent government IDs greatly reduces the chances of having to mitigate fraud later.

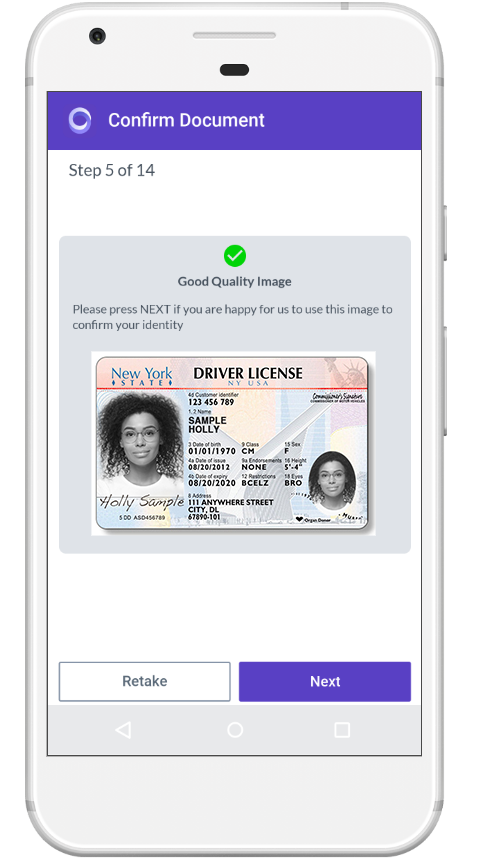

Once the driver’s license images are captured, OneSpan uses AI and advanced authenticity algorithms to analyze the image of Holly’s driver’s license. This produces an authenticity score to determine if Holly’s license is fraudulent or authentic.

The solution can then layer in additional authentication checks such as facial biometrics or fingerprint biometrics to further verify the applicant’s identity.

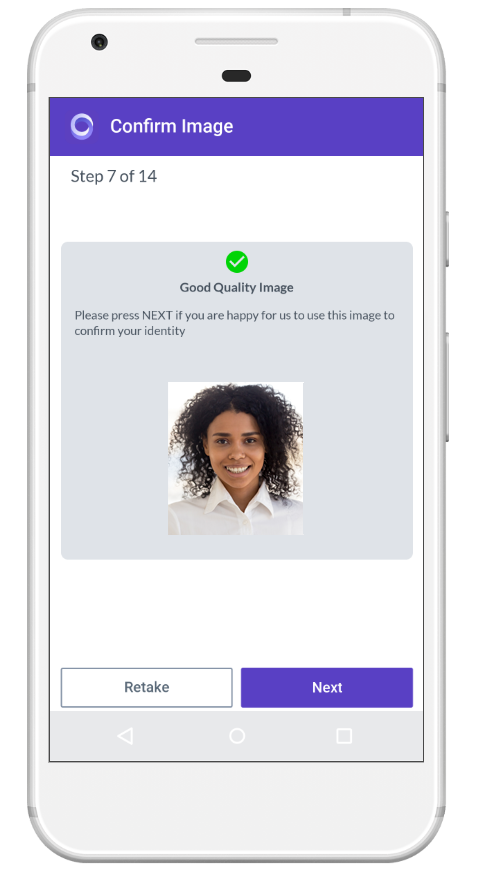

In this scenario, Holly is asked to further verify her identity using facial comparison. Easy enough – she just takes a selfie.

Behind the scenes, OneSpan’s Secure Agreement Automation solution extracts Holly’s biometric data from the selfie and compares it to the image in the authenticated driver’s license to determine if she is physically present and that she is who she claims to be.

Passive liveness detection can also be applied to Holly’s selfie to prove genuine human presence. Liveness detection helps to prove that an image has not been fraudulently created using methods such as high-resolution print-outs or pre-recorded videos.

These digital identity verification methods verify that Holly’s identity documents are genuine and that Holly is who she claims to be. These steps help to mitigate application fraud from occurring.

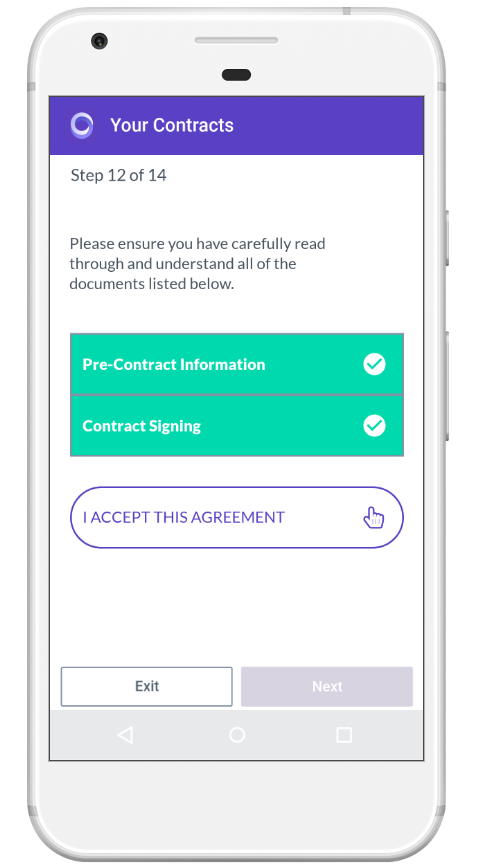

The next step in the new account opening process is for Holly to review, sign and execute the account agreement terms.

Electronic Signature Used to Create An Enforceable Digital Agreement

Once Holly’s identity has been validated digitally, the bank presents the pre-contract information and completed application for electronic review and signing.

Because OneSpan Secure Agreement Automation seamlessly combines identity verification and e-signature capabilities, it captures Holly’s personal data from her driver’s license and automatically imports it into the application form.

At this point, OneSpan enables Holly to electronically review and sign the new account agreement.

Once the agreement has been reviewed by Holly, she simply “taps to sign” and submits her completed application.

Behind the scenes, OneSpan creates an electronic audit trail of the entire account opening process, capturing every screen that Holly sees and every action she takes. The audit trail ensures that the financial institution has a detailed record of the digital process including both the digital identity verification and e-signature steps.

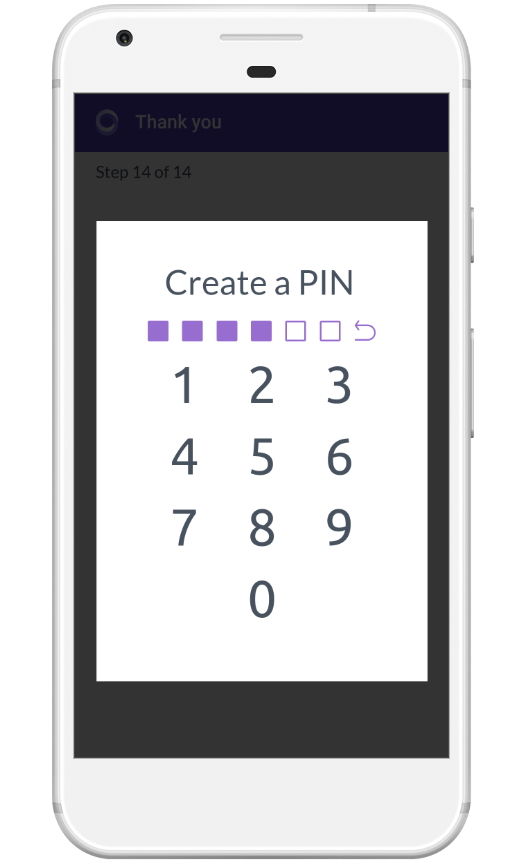

Trusting Holly’s Mobile Device

Now that the application is signed and executed, Holly’s smartphone is registered so that OneSpan and the bank can recognize it as a trusted device. This means that Holly will be authenticated smoothly when she uses the bank’s mobile application for everyday banking.

To do this, Holly creates a secure 6-digit PIN number and submits it to the bank. Once her mobile device is accepted by the bank, the mobile device is now trusted and automatically synced with her new savings account.

Holly’s application is now successfully completed. It took just minutes to open her new account.

With Holly’s new account opened, she is free to add funds and continue with the standard onboarding process offered by her financial institution. More importantly, from prospect to new customer, Holly was able to complete the account opening process completely remotely and through digital channels. This provides the maximum possible convenience and flexibility.

Driving Down Identity and Application Fraud

Financial institutions need to drive down instances of application fraud. Digital identity verification can enable financial institutions to mitigate application fraud while providing a more positive customer experience. With automated identity document verification and facial comparison, banks can validate customer’s identity in real-time, whether the transaction takes place online or via a mobile device, as demonstrated in this real-life scenario.

Digital identity verification not only helps FIs prevent application fraud – it can also help financial institutions fulfil Know Your Customer (KYC) and anti-money laundering (AML) compliance requirements.

Secure agreement automation using digital identity verification, e-signature and digital audit trails also allows banks and FIs to create legally enforceable and compliant agreements. With a full digital audit trail, banks and FIs can prove to external or internal auditors that they followed a consistent and compliant process when onboarding a new customer.

White paper

Rethink digital account opening for faster growth

Successfully onboarding a new customer on their first attempt accelerates time-to-revenue and customer loyalty. Learn best practices from peers who transformed digital account opening.

Read now